A new Forbes analysis of 157 crypto exchanges finds that 51% of the daily bitcoin trading volume being reported is likely bogus.

ithin the emerging and turbulent market for cryptocurrencies, where there are no fewer than 10,000 tokens, bitcoin, is the great granddaddy, the blue-chip, representing 40% of the $1 trillion in crypto assets outstanding. BitcoinBTC 0.0% is crypto’s gateway drug. An estimated 46 million adult Americans already own it according to New York Digital Investment Group, and an increasing number of institutional investors and corporations are warming to the nascent alternative asset.

But can you trust what your crypto exchange or e-brokerage reports about trading in the most important digital currency?

One of the most common criticisms of bitcoin is pervasive wash trading (a form of fake volume) and poor surveillance across exchanges. The U.S. Commodity Futures Trading Commission defines wash trading as “entering into, or purporting to enter into, transactions to give the appearance that purchases and sales have been made, without incurring market risk or changing the trader’s market position.” The reason why some traders engage in wash trading is to inflate the trading volume of an asset to give the appearance of rising popularity. In some cases trading bots execute these wash trades in tokens, increasing volume, while at the same time insiders reinforce the activity with bullish remarks, driving up the price in what is effectively a pump and dump scheme. Wash trading also benefits exchanges because it allows them to appear to have more volume than they actually do, potentially encouraging more legitimate trading.

There is no universally accepted method of calculating bitcoin daily volume, even among the industry’s most reputable research firms. For instance, as of this writing, CoinMarketCap puts the latest 24-hour trading of bitcoin at $32 billion, CoinGecko at $27 billion, Nomics at $57 billion and Messari at $5 billion.

Loading...

Adding to the challenges are persistent fears about the solvency of crypto exchanges, underscored by the public collapses of Voyager and Celsius. In an exclusive interview with Forbes in late June, FTX CEO Sam Bankman-Fried commented that there are many exchange bankruptcies yet to come.

A significant repercussion of this lack of faith in its underlying markets is the Security and Exchange Commission’s refusal to approve a spot bitcoin ETF.

Unfortunately for the bitcoin ETF hopefuls, many of these fears and criticisms are valid. As part of Forbes research into the crypto ecosystem using 2021 data, we ranked the 60 best exchanges in March. More recently we conducted a deeper-dive into the bitcoin trading markets to answer a few pressing questions:

- Where is bitcoin traded?

- How much bitcoin gets traded every day?

- How is bitcoin traded?

Our study evaluated 157 crypto exchanges across the world. Here are our main findings:

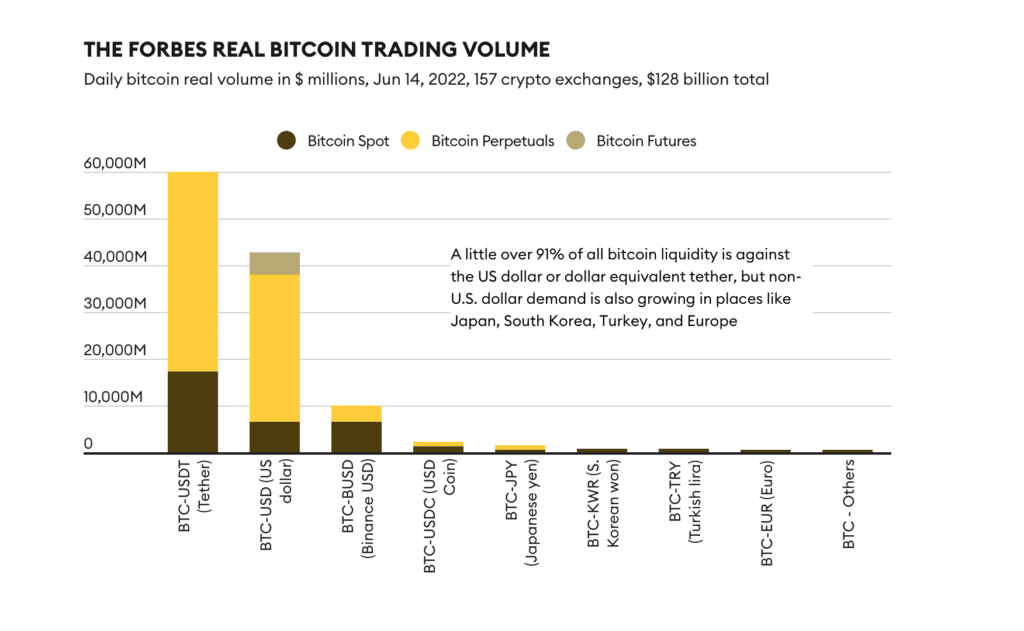

- More than half of all reported trading volume is likely to be fake or non-economic. Forbes estimates the global daily bitcoin volume for the industry was $128 billion on June 14. That is 51% less than the $262 billion one would get by taking the sum of self-reported volume from multiple sources.

- TetherUSDT 0.0%, the world’s largest stablecoin, continues to be a dominant player in the crypto trading economy, especially when it comes to trades against bitcoin. Its current market capitalization is $68 billion, despite questions about its reserves.

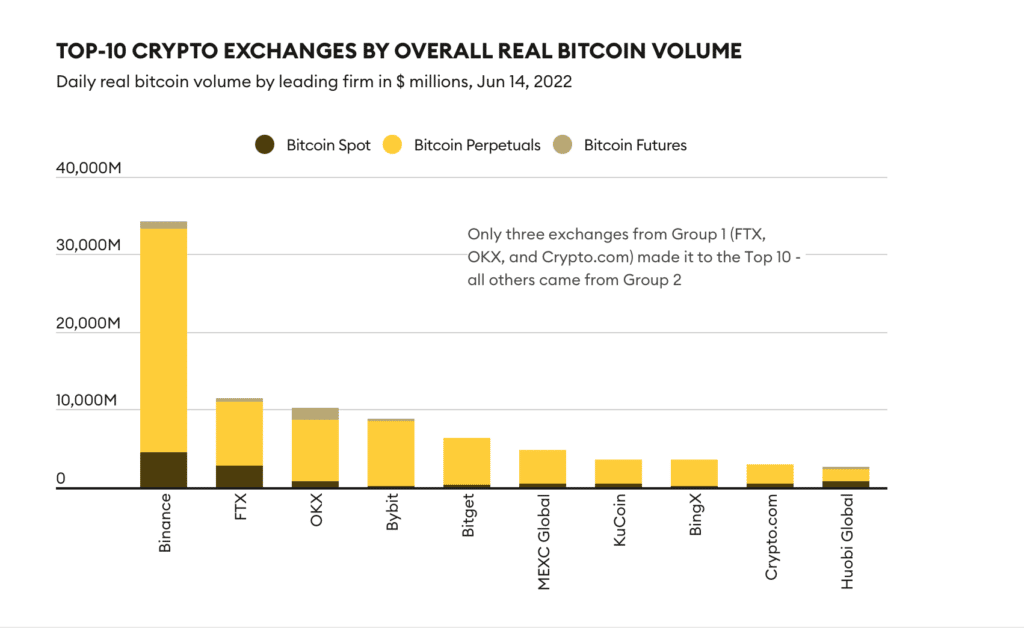

- In terms of how much bitcoin activity takes place at these firms, 21 crypto exchanges generate $1 billion or more in daily trading activity, while the next 33 exchanges had volume between $200 million and $999 million across all contract types, spot, futures and perpetuals. Perpetual futures, or perpetual swaps as they are also known, are futures contracts that don’t require investors to roll over their positions. Binance is the clear leader, with a 27% market share, followed by FTX. Looking only at spot bitcoin, the top position is shared by Binance, FTX, and OKX. Chicago-based CME Group is the market leader in bitcoin futures trading.

- The biggest problem areas regarding fake volume are firms that tout big volume but operate with little or no regulatory oversight that would make their figures more credible, notably Binance, MEXC Global and Bybit. Altogether, the lesser regulated exchanges in our study account for approximately $89 billion of the true volume (they claim $217 billion).

- The creation of new trading assets and products such as stablecoins and perpetual futures adds complications for national authorities seeking to regulate crypto markets. Major U.S. exchanges hardly utilize these instruments or contracts in any of their trading. However, offshore exchanges make significant use of them as ways to synthetically create U.S. dollar liquidity on their platforms (they cannot get U.S. bank accounts).

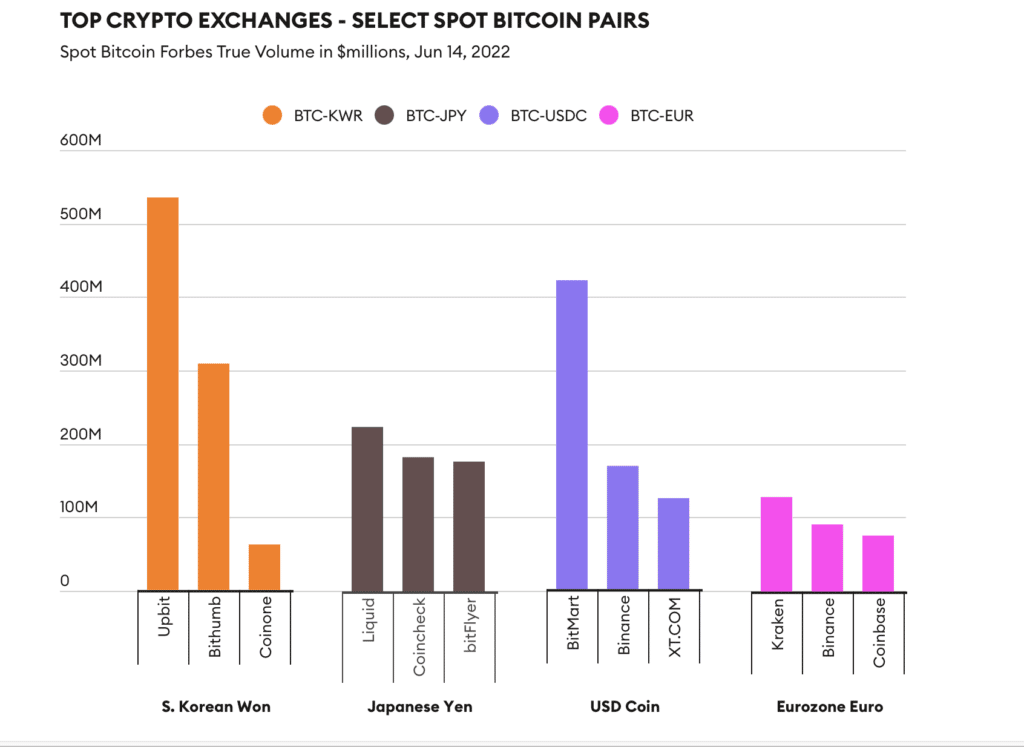

- In the Western world and particularly in the U.S., it is tempting to think of bitcoin only trading against either the U.S. dollar or the euro and British pound. But some of the largest trading pair activity occurs against fiat currencies like the Japanese yen and Korean won and against major stablecoins like Binance U.S. dollar and the USD coin.

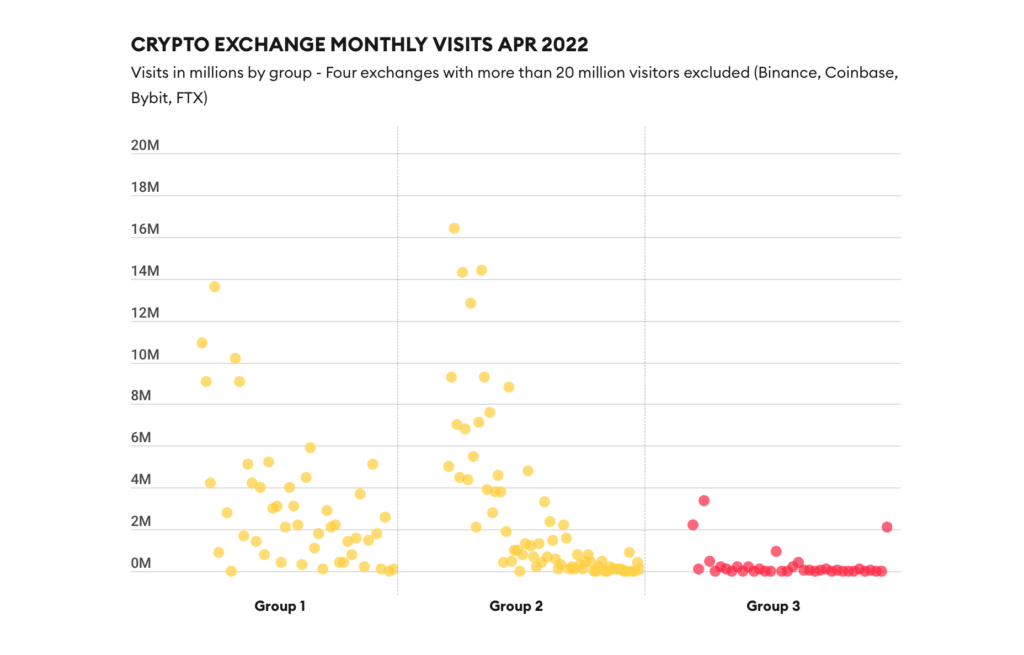

- 573 million people visit crypto exchange websites on a monthly basis.

We hope that this report builds on top of the important work done by other digital asset researchers such as Bitwise, which estimated in a March 2019 white paper that 95% of CoinMarketCap’s bitcoin trading volume was fake and/or non-economic.

Our Approach

Forbes uses quantitative and qualitative analyses to adjust trading volume reported by the exchanges. Unlike other methods that carry out tests on transactional data (and can also be duped), Forbes grades a firm’s credibility by evaluating no fewer than five datasets that together inspire or diminish confidence in a firm’s self-reported data. Data comes from four crypto media firms, CoinMarketCap, CoinGecko, Nomics and Messari, as well as multiple exchanges and two other third-party data providers.

We apply volume discounts based on a proprietary methodology that relies on 10 factors such as an exchange’s home regulator if any and volume metrics based on an exchange’s web traffic and estimated workforce size. We also use the number and quality of crypto licenses as proxy to gauge the sophistication of each crypto exchange in matters pertaining to regulation and trade surveillance. If a firm shows a commitment to transparency by conducting token proofs of reserve or by participating in Forbes crypto exchange surveys, it qualifies for a “transparency credit” that lowers any discount that may otherwise apply.

Many of these factors were also present in Forbes’ crypto exchange ranking formula. We divided them into three categories:

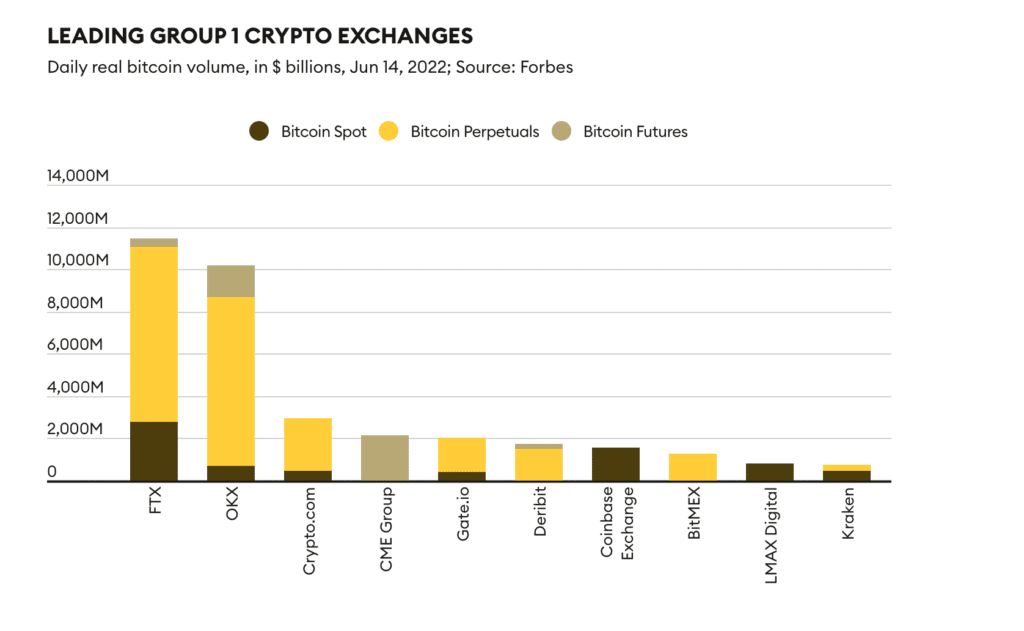

Group 1: 49 crypto exchanges that were assigned discounts of 0-25% generated $39 billion of real bitcoin trading activity across all markets–spot, derivatives and futures–on June 14.

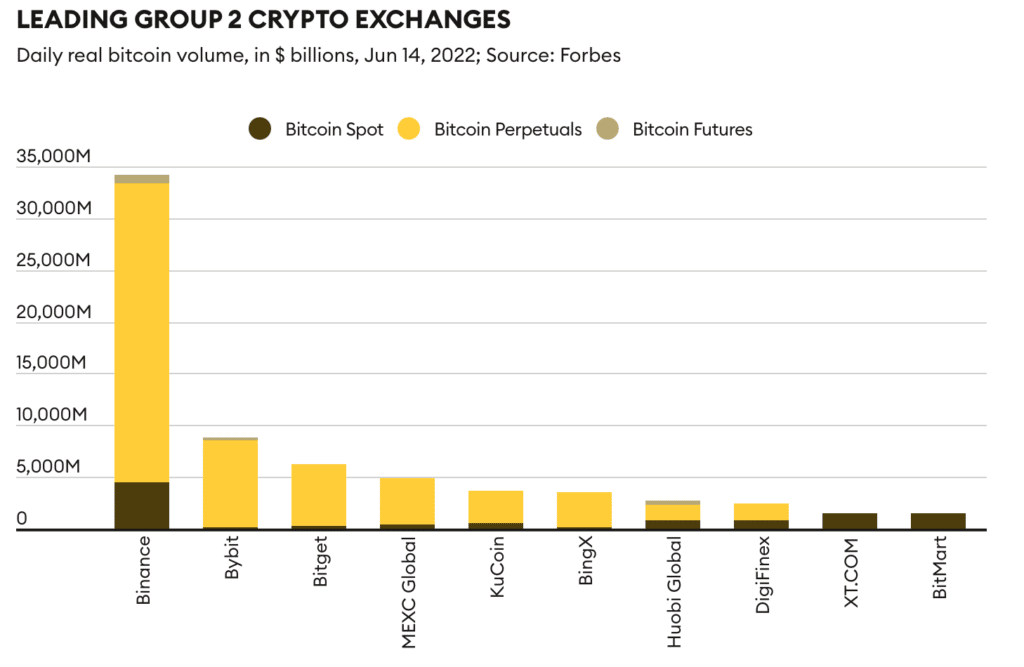

Group 2: 73 exchanges with volume discounts of 26% to 79% generated $81 billion in transactional activity (vs. $158 billion claimed)

Group 3: The remaining 35 firms were penalized with a high discount rate (80-99%) and traded $7.7 billion out of $59 billion claimed.

SUMMARY CHARTS & TABLES

Despite crypto’s global nature, spot bitcoin trading activity is centered around relatively few currency pairs and stablecoins. Stablecoin USDT is the biggest, followed by the U.S. dollar. The next biggest fiat assets are the yen and won.

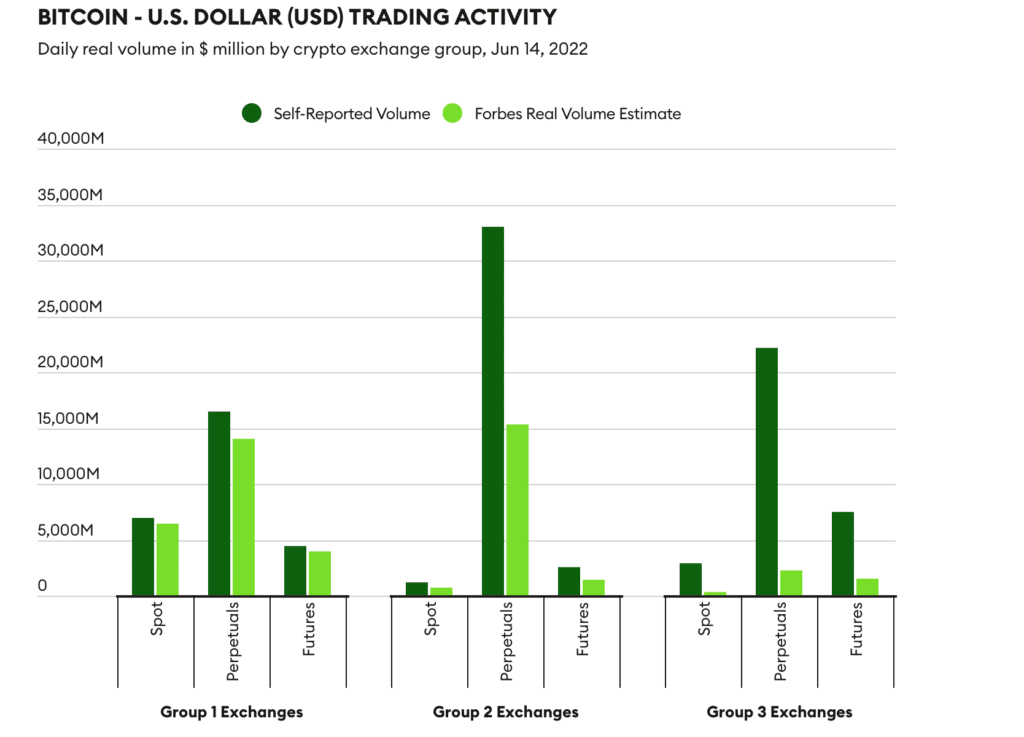

BTC-US DOLLAR Daily Volume

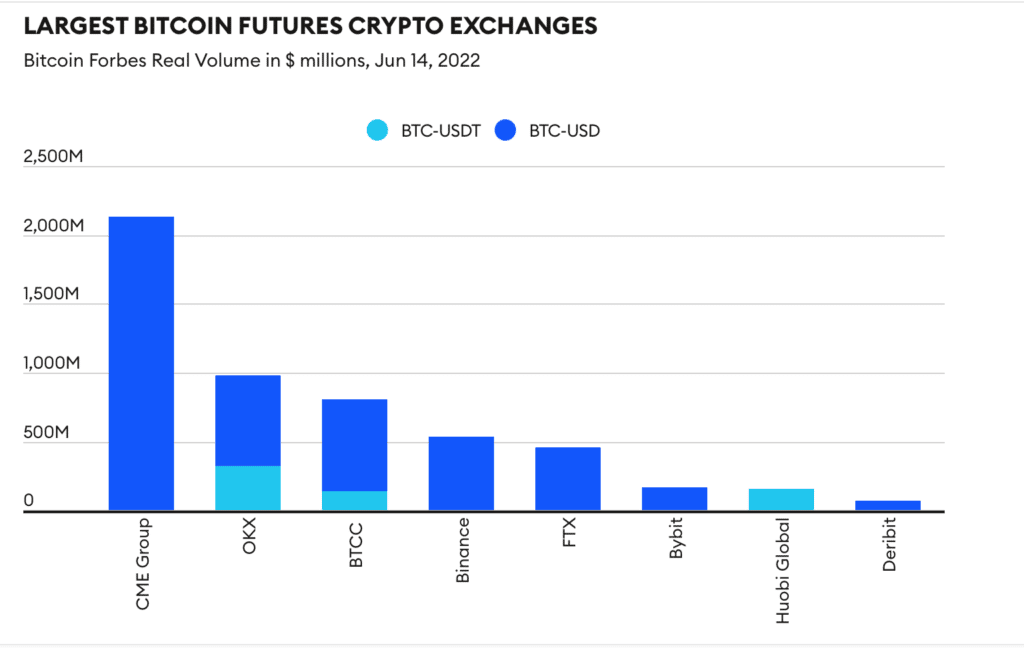

Group 1 exchanges, many of which are based in the U.S., provide $24.3 billion in daily USD-BTC liquidity, and Group 2 exchanges add $17.3 billion. The prominence of Group 1 exchanges as the main source of BTC-USD occurs across spot, perpetuals, and futures contracts. CME Group is the leading provider of bitcoin futures globally, with $2.1 billion of USD-BTC futures changing hands daily. There are at least 27 crypto exchanges–12 in Group 1–that have daily BTC-USD liquidity greater than $5 million.

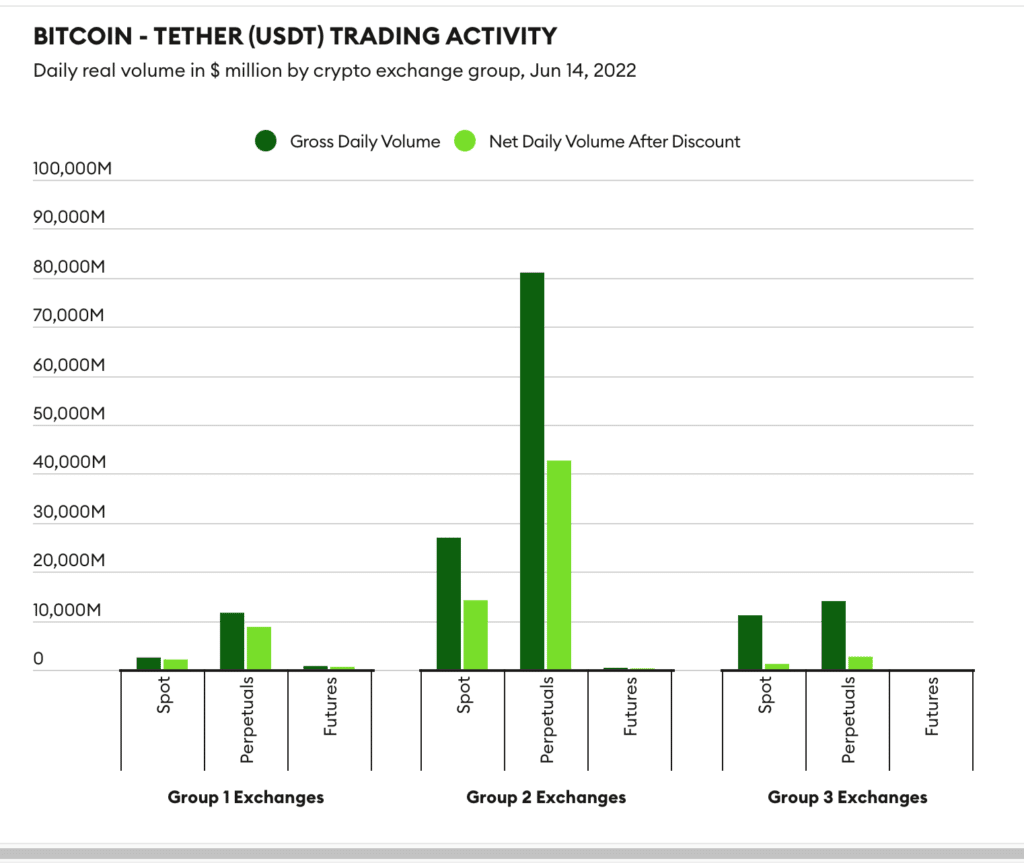

BTC – U.S. TETHER Daily Volume

At $71.4 billion daily volume, bitcoin-tether (BTC-USDT) activity exceeds that of BTC-USD by 57%, with 79% generated by Group 2 crypto exchanges and 5% by those in Group 3. There are 77 exchanges–44 in Group 2, 12 in Group 1–with daily bitcoin-tether volume above $5 million. Tether is prominent across spot and perpetual futures markets, less so among the regulated futures industry, which is largely absent outside of the U.S.

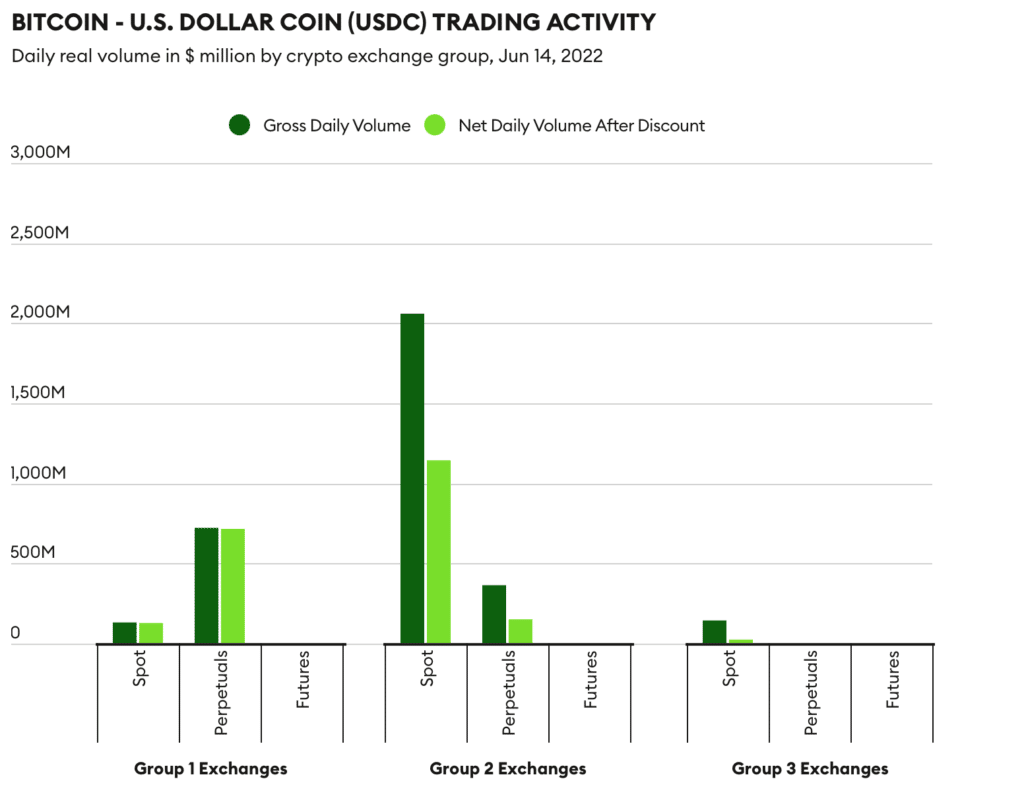

BTC – U.S. DOLLAR COIN Daily Volume

U.S. dollar coin (USDCUSDC 0.0%) is gaining adoption in the stablecoin arena. Daily liquidity for bitcoin-USDC was $2.15 billion, with Groups 1 and 2 splitting that total 39% and 60%, respectively. An interesting observation is that Group 2 exchanges use USDC actively in the spot bitcoin market whereas Group 1 exchanges do so with perpetuals. This different use could suggest that Group 2 exchanges may be open to the idea of supporting an alternative to tether’s dominance in the stablecoin market.

USDT and Binance USD (BUSDBUSD 0.0%) each generate more volume than USDC, but the latter now has 26 crypto exchanges (17 in Group 2) with daily trading volume of $5 million or more, versus 77 exchanges for USDT and five with BUSD. If tether’s prominence begins to wane, USDC could be the stablecoin most likely to pick up its crown.

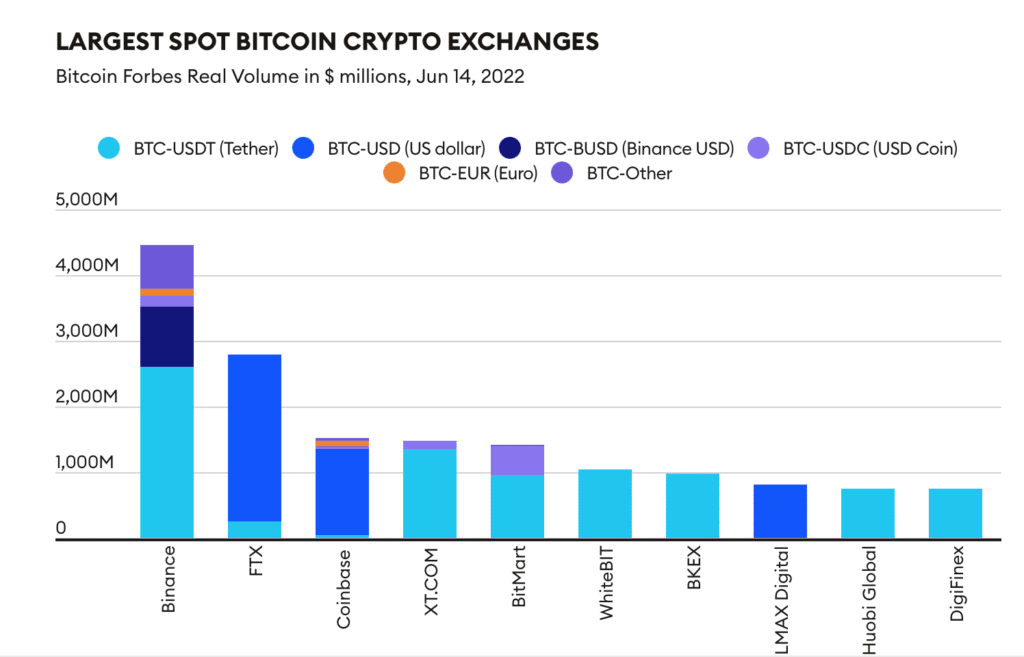

CRYPTO EXCHANGES BY REAL TRADING VOLUME

Bitcoin Trading Volume by Exchange Group

The top-10 Group 1 crypto exchanges by volume originate from across the world, with three from the U.S. (CME Group, Coinbase, Kraken), one from Singapore (Crypto.com), one from Europe (LMAX Digital), four from financial offshore centers (FTX, OKX, Gate.io, BitMEX), and one from Central America (Deribit).

Among Group 1 firms, FTX is the largest and growing at a fast clip. It wasn’t until mid 2021 when institutional funding fueled a transformation of FTX operations from a midsized unregulated exchange focused on offshore crypto derivatives to a global group of exchanges today regulated in the U.S., Japan, Europe and elsewhere. In addition to derivatives, FTX trades in crypto spot, tokenized stocks and has recently added equities.

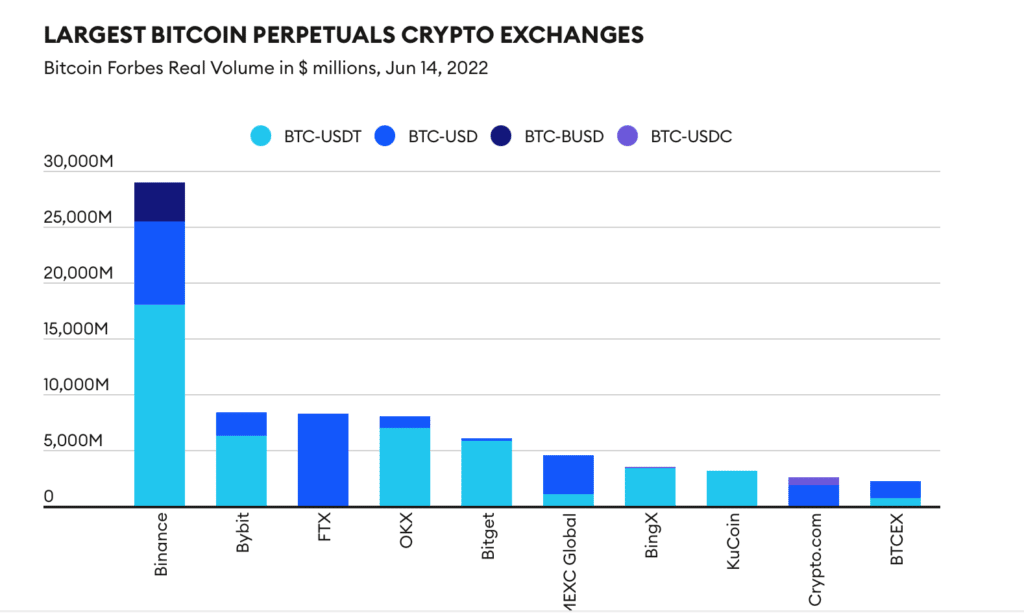

Group 2 crypto exchanges tend to be large and possess wide product offerings. They primarily focus on growth and tend to have much less interest in being regulated where they operate. They also generally lack robust ways to track and deter wash trading. Binance is by far the largest crypto exchange in Group 2, with $34.2 billion of daily trading activity followed by Bybit with $8.9 billion. The majority of these exchanges are based in offshore havens such as the Seychelles and British Virgin Islands.

Group 3 consists of 36 crypto exchanges which, with few exceptions, are unregulated and small. Their huge self reported volume and tiny visitor number cast doubt on the possibility that a limited audience could indeed generate that much trading activity. A case in point is BitCoke, which CoinMarketCap identifies as a Hong Kong-based, Cayman Island-domiciled exchange that purportedly generated $14 billion daily–mostly from BTC-USDT perpetuals. SimilarWeb, however, indicates that the exchange’s domain receives less than 10,000 monthly visitors–with 53% coming from Argentina alone. The discrepancies in volume versus traffic plus lack of regulatory credentials result in Forbes discounting this firm’s volume by 95% to $702 million.

LARGEST EXCHANGES BY MAJOR BITCOIN PAIR

As discussed above, BTC/USD and BTC/USDT are by far the biggest spot pairs for bitcoin, but there are a few other pairs worth mentioning. The next largest are BTC-KWR, BTC-JPYPY-1.3%, BTC-USDC, and BTC-EUR. An exchange’s decision to offer base assets across bitcoin, especially when it comes to fiat, usually comes down to the local fiat currency used by an exchange’s client base. Each of the companies trading bitcoin against the won or yen are based in South Korea or Japan respectively. USDC, by nature of its blockchain-based DNA, is easier to cross national-boundaries. Readers may notice that Kraken, Binance or Coinbase are not based in Europe, though they each have a series of licenses to operate in certain countries. They each offer euro trading as a way to onboard new users, but unlike the South Korea or Japan-based exchanges, the euro is not their most dominant base asset for trading.

However, while eight pairs by volume garner the majority of bitcoin volume, there are dozens of other varieties trading at obscure exchanges uncounted even in our present study. For example, it is difficult to find the amount of BTC-NGN (Nigerian naira) volume traded in Nigeria because crypto data firms like Nomics, CoinMarketCap and CoinGecko generally do not track it. One can safely assume that local crypto exchanges not widely known outside of Nigeria capture most BTC-NGN liquidity, which is likely true for many other exchanges operating in emerging markets.

These observations are largely true when it comes to perpetual futures as well. However, the won and the yen do not appear to have gained significant market share in this area.

Finally, when it comes to the traditional futures markets, such as those that offer regular monthly expirations, the only two pairs that seem to matter are BTC-USD and BTC-USDT.

KEY TAKEAWAYS

The Forbes Real Volume study revealed a number of key insights for crypto investors and industry.

Bitcoin may just be the beginning of the problem. If reported trading volumes for bitcoin, the most regulated and closely-watched crypto asset around the world, are untrustworthy, then metrics for even smaller assets should be taken with even greater grains of salt. At its best, trading volume is one of the most measurable signs of investor interest, but it can be easily manipulated to convince novice investors that it has much more demand than it actually does.

Binance remains the 800-lb elephant in the room. Even after a 45% discount on its volume, Binance still generates the equivalent of 27.3% of all “real” trading volume. There is no other crypto exchange that can match its market power, and it’s been that way for the past two years. That said, while Binance has been saying all of the right things about cooperating with regulators – it has started getting licenses around the world and is promising to announce a global headquarters – questions remain about its operational controls. Unless regulators can get comfortable with Binance’s legitimacy, it may be difficult to envision a spot ETF getting approved anytime soon.

Tether remains “Too Big To Fail” – for now: This study invites more questions about the true use and value of two of the largest stablecoins – USDT and BUSD. Say what you will about Tether, and people have, it has found product-market fit in a big way. But that is the exact problem in the minds of many so-called Tether Truthers, who do not believe that the $68 billion is actually backed by reserves. It is hard to imagine what would happen to markets if traders stopped trusting tether – and to be fair there is little evidence that this is happening – and none of its competitors were willing to take its place.

Areas For Future Study

The role of stablecoins in market manipulation. We did not see any evidence that tether-based trading pairs were any more prone to fraud than other assets. However, this area is worth looking into further, especially if tether begins to deviate again from its $1 peg or other algorithmic stablecoins begin to gain traction in large spot-market trading. An ostensibly stable base asset that has higher-than-expected volatility can always lead to both legitimate arbitrage opportunities as well as openings for fraud.

The potential of perpetual futures to be manipulated. Through our research, including first-person interviews with direct market participants, we did not see any evidence that perpetual futures are more prone to wash trading and other forms of manipulation than conventional futures or spot contracts. However, given the relatively novel nature of this product (it was created in 2016), as well as its dominance in crypto trading, it is well worth deeper study.

The future of DEXS in market manipulation. This report did not focus on decentralized exchanges (DEXs), in large part due to the fact that they are not major players in bitcoin trading. To the contrary, when it comes to spot markets most of the major players have separated themselves from the major centralized exchanges by specializing in novel ways to provide liquidity in long-tail assets that are not financially worthwhile for many traditional exchanges to offer. That said, the market share of DEXs has slowly been creeping up to that of spot–there are even days where Uniswap, the largest DEX, has more trading volume than Coinbase.

FORBES METHODOLOGY

The Forbes methodology for discounting bitcoin trading volume follows a series of steps.

Regulation. We identify crypto licenses and from what regulatory body that each exchange possesses and use that as proxy to gauge their level of sophistication and intent to deter wash trades and publishing fake volume.

Third-party input. We considered the work of select third parties such as volume data from CoinMarketCap, CoinGecko, Nomics and Messari. Messari’s volume statistics are less extensive by pairs, and it has fewer exchanges than its peers, but it has its own real-volume calculations. Forbes tracked in recent months how Messari applied a volume discount ranging from 40% to 65% to Binance volume, compared with the averages reported by CoinMarketCap, CoinGecko and Nomics at the time. Messari also discounts the trading volume of FTX by a lesser percentage (less than 20%) and that of Kraken by 99%. With regards to this latter, Forbes doesn’t share the view of applying a heavy discount to a firm that is among the most regulated crypto exchanges in the world. Most exchanges going through the Messari real volume analysis, however, lack any type of volume discount.**

Web traffic. Forbes employs third-party data from web analytics firm SimilarWeb to heavily discount the volume of firms claiming a high trading volume without having sufficient crypto licenses and web traffic to generate such volume.

Forbes interviews. Forbes has conducted dozens of interviews of senior executives at major crypto exchanges to supplement quantitative information on a firm’s profile.

* Editor’s note. After publication, Bullish.com provided Forbes non public information, such as that Bullish is in the process of moving to an institutional-only focus from the present one which appears to be retail and institutional. For the original ranking Bullish received a discount of 90% on bitcoin volume, however considering its institutional focus and other factors a discount of 15% is more appropriate.

** Editor’s note II. After publication, Messari notified Forbes that parts of its website experienced a glitch (now resolved) showing only a subset of Kraken’s trading volume; the firm also reaffirmed that it does not discount the volume of Kraken, FTX, or Binance.

By Javier Paz, Forbes Staff

Loading...